Where traditional lead enrichment software falls short for wealth managers

Download the LLM 2026 Prompting Guide

Teach your AI to think like your firm with 10+ customizable prompts

Download TodayAccording to industry benchmarks, companies using lead enrichment data can generate up to 2x more qualified leads, because the software is built to answer a specific question: does this person work at a company that fits your ideal customer profile, and do they have the authority to make a purchase? That question maps perfectly to B2B sales. It is the wrong question for wealth management, where an AI wealth management tool needs to evaluate individuals against an entirely different set of criteria.

Wealth managers are not qualifying companies. They are qualifying individuals. The question is not whether someone's employer meets a revenue threshold or whether their title suggests budget authority. It is whether this specific person has the financial complexity, household context, and wealth profile that fits the kind of advisory relationship your practice provides. That is the profile that generates warm leads for financial advisors, not company revenue or org chart position.

B2B lead enrichment software was built to answer the first question with precision. It has no framework for answering the second. The data it carries, the signals it tracks, and the definition of "qualified" it applies are built around a buyer your practice is not chasing. A purpose-built prospecting tool for financial advisors starts from the opposite premise.

The qualification question B2B enrichment was built to answer

B2B lead enrichment exists because enterprise sales teams needed a faster way to decide which prospects deserved time and attention. The answer they built was elegant: filter by company fit first, then confirm contact authority. Surface the names that pass both tests. Skip the rest.

It works for the use case it was designed for. The logic is coherent because the underlying assumption is coherent: you are selling to organizations, so organizations are the primary unit of analysis. Every enrichment attribute flows from that starting point.

How the B2B qualification filter works

A qualified B2B lead typically passes two layers of filters. The first is company-level: industry, headcount, revenue range, funding stage, technology stack. The second is contact-level: does this person hold a title that typically controls budget for this kind of purchase?

The enrichment data that populates those filters is professional and firmographic. It is a coherent system precisely because the goal is coherent. You are looking for the right person at the right company. The data is built to tell you that.

Why the same filter produces the wrong answer for wealth management

Apply the same logic to wealth management prospecting and the breakdown is immediate. A contact who is a senior director at a 200-person company clears most B2B qualification filters with no problem: right company size, right title tier, verified email, confirmed employment. By B2B enrichment standards, that contact is qualified.

What you still do not know: whether they have investable assets, what their household looks like financially, whether they are already working with an advisor, or whether their career has generated the kind of wealth that creates a real planning need. The B2B filters confirmed the contact exists and has a professional title. They said nothing about whether this person is a wealth management prospect.

What wealth management lead qualification actually requires

The qualification criteria in wealth management are personal, not organizational. Advisors need to know things about a person's financial life that never appear in any professional directory, because those things have nothing to do with where someone works.

This is not a gap B2B enrichment tools can close with more data or better coverage. It is a question of what type of data qualifies a prospect in the first place, and that type is consumer-side: drawn from property records, equity filings, and household data rather than from professional networks and company databases.

Estimated net worth as the first qualification signal

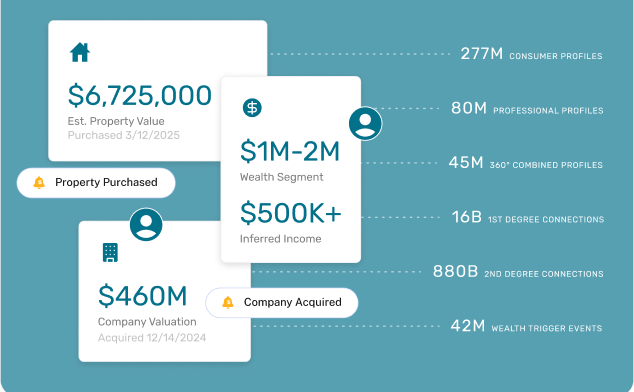

Estimated net worth derived from public records is the most direct qualification signal in wealth management. Property values, real estate holdings, and equity positions from public filings combine to produce an approximate picture of household wealth that is, in practice, more useful to an advisor than any firmographic data point.

A wealth manager who knows a prospect owns two investment properties and holds a meaningful equity position in a public company can make a real judgment about fit before any outreach happens. That judgment is where the prospecting process actually starts. Without it, the list is a list of names, not a list of prospects. Platforms built for financial advisor prospecting treat net worth estimates as a first-pass qualification filter, not an afterthought.

Household context over company context

Company context tells you who the prospect's employer is. What it cannot tell you is who else is in the household, whether there is shared estate complexity worth addressing, or whether the financial decisions in that household are made individually or jointly. Those factors shape the nature of the advisory relationship an individual actually needs.

A single high earner with a concentrated equity position needs a different conversation than a dual-income household managing inherited wealth and real estate. B2B enrichment carries neither piece of context. Consumer-layer enrichment puts both on the table. For advisors building around financial advisor lead generation that converts, household context is one of the first filters that separates a real prospect from a professional contact.

Career trajectory as a wealth indicator

Current employer is a proxy, not a qualifier. What matters for HNW prospecting is the financial dimension of someone's career: tenure at a high-growth company, equity compensation structure, a professional arc that points toward meaningful wealth accumulation.

Two people with identical job titles at comparable companies can have completely different wealth profiles depending on when they joined, what they were compensated with, and where the company is in its growth cycle. Standard enrichment confirms the title and moves on. Wealth-specific enrichment asks what that career has actually produced for the individual, and that is a question professional data cannot answer.

Why consumer-layer data isn't in most enrichment platforms

Most lead enrichment platforms are built around professional databases and company records because that is what their buyers need. B2B sales teams are not asking about property values or household composition. They have no use for equity filings or net worth estimates. Those data types simply have no place in the product.

The absence of consumer-layer data from most enrichment platforms is not an oversight. It is a feature of the market those tools were built to serve. The demand for that data does not come from SaaS sales teams, so the supply was never developed for them.

Where consumer-layer data actually comes from

Property records, equity holdings, and household data come from a different set of public filings than professional databases index. County assessor records, SEC filings, public property transfers, and household data registries are the sources. They exist. They are updated. They are not difficult to access in aggregate.

The challenge is that sourcing and maintaining them at scale requires building a data infrastructure specifically for that purpose. It is not something you can layer onto a B2B enrichment platform as an add-on, because the underlying data architecture is different. Platforms focused on financial advisor prospecting tools are purpose-built around these sources, not retrofitted to include them.

The coverage problem at the individual level

Individual-level coverage also looks different from company-level coverage. A B2B enrichment platform can achieve strong coverage of mid-market and enterprise companies because those companies have public footprints: press coverage, job postings, LinkedIn presence, funding announcements. Finding them is not hard.

Many high-net-worth individuals are not prominent in professional databases. Business owners who have not raised institutional capital, inheritors who are not executives at known companies, high-net-worth professionals in non-public roles: these are real prospects for a wealth management practice who do not appear in the places B2B enrichment tools go looking. Consumer-layer coverage accounts for this in ways that professional data coverage cannot. The wealth management prospecting tools built for this use case index across all of those surfaces.

How Aidentified approaches HNW lead enrichment

Most lead enrichment tools were designed for B2B sales, so they verify titles and company details but miss the financial signals wealth managers actually need. Aidentified helps advisors qualify prospects with consumer-level data like estimated net worth, household composition, and equity holdings, so outreach starts with stronger opportunities.

Most advisors who switch to consumer-layer qualification find their prospect list reshuffles significantly, with prospects strong on paper moving down and genuine financial profiles moving up. If you're ready to qualify your prospects on the financial criteria your practice actually uses, try Aidentified for free.

FAQs: lead enrichment software for wealth managers

How is lead enrichment different from lead generation?

Lead generation finds new prospects and brings them into your pipeline. Lead enrichment determines whether those prospects are actually qualified for your practice and what financial context exists before outreach begins. For wealth managers, enrichment is where the real qualification work happens: it surfaces household profile, estimated net worth, and equity holdings that tell you whether a contact is a real prospect or just a name with a professional title.

The distinction matters for how you allocate prospecting time. Generation broadens the top of the funnel. Enrichment narrows it to the names worth pursuing. Platforms built for financial advisor lead generation combine both layers to produce shorter, more actionable lists rather than longer generic ones.

What makes a lead qualified in wealth management?

In wealth management, a qualified prospect has a financial profile that matches the complexity your practice serves, and a life stage where advisory services are genuinely relevant. That means estimated net worth above your practice's threshold, household composition that creates planning complexity, and career or asset context that points toward a real financial need.

None of those qualification criteria appear in a standard B2B enrichment database. They require consumer-layer data sourced from property records, equity filings, and household data. Advisors focused on prospecting high-net-worth clients need enrichment built around those sources, not around firmographic fit.

Why don't standard B2B enrichment tools work for wealth management?

The qualification logic embedded in B2B tools does not apply to individual financial prospects. B2B tools determine fit by analyzing a company's profile and a contact's role within it. Wealth management fit is determined by an individual's personal financial profile, which no company database tracks.

A contact can pass every B2B qualification filter and still have no investable assets. One can fail every filter and be exactly the kind of high-net-worth individual your practice is built to serve. For a broader look at building a practice around the right qualification signals, see this guide on how to get clients as a financial advisor.

How do wealth managers use lead enrichment differently than B2B sales teams?

B2B sales teams use enrichment to confirm company fit and contact authority before investing sales time. The qualification question is organizational: does this company fit our ideal customer profile, and can this person sign a contract?

Wealth managers use enrichment to answer a personal question: does this individual have the financial profile that creates a genuine advisory need? That requires household wealth context, equity exposure, and career depth that professional databases do not carry. The prospecting framework for financial advisor prospecting is built around that personal qualification question from the first step, not as a follow-on to a company-fit filter.

growth engine with the

LLM Prompting Guide.

Reveal the power of your network with Aidentified’s industry-leading AI.

Discover how Aidentified can transform your specialty services business. Contact us today for a personalized consultation and demo.

Explore a demo