5 Financial advisor prospecting ideas to build leads

This is a div block with a Webflow interaction that will be triggered when the heading is in the view.

Increase your financial advisor pool of candidates

Join thousands of financial advisors leveraging AI-powered relationship intelligence.

Try for free today!TL;DR

Financial advisor prospecting ideas that work share one trait: they reach the right prospect after a wealth event, not on a fixed schedule.

The life events that most reliably open a financial planning conversation include liquidity events, senior role changes, significant inheritance, and business sales.

Warm introductions, COI referrals, and LinkedIn outreach all convert better when tied to a specific event in the prospect's life rather than deployed without one.

A monitoring system that tracks wealth events across your prospect list turns a reactive approach into a proactive one.

Most financial advisor prospecting ideas focus on the channel: more calls, better LinkedIn messages, smarter follow-up sequences. The problem is rarely the channel. On the contrary, real progress on client acquisition for financial advisors often comes from fixing timing.

Financial decisions aren't made on a fixed schedule. People don't decide they need a new financial advisor on a random Tuesday because they got a well-crafted email. They decide after an important shift in their financial lives: a job change, a business sale, an inheritance, or a real estate transaction. That's when the question of who manages their wealth becomes a priority, and exactly what a wealth event monitoring platform, powered by ai for financial advisors, is built to surface before the window closes.

Advisors who reach out during that window convert at a significantly higher rate than those who reach out three months before or six months after.

Financial advisor prospecting ideas covered in this guide

This guide covers 5 financial advisor prospecting ideas, ranked from the foundational concept to the tools that make it scalable:

- Prospecting as a financial advisor starts with one question

- Wealth events that create the best financial planning conversations

- Warm introductions, COI referrals, and LinkedIn outreach all improve with timing

- Monitor your prospect list for wealth events at scale

- Apply a timing checklist before every prospecting outreach

5 Financial advisor prospecting ideas ranked by impact

1. Start with the right timing signal

Right now, only a small number of your prospects have had something happen that makes them ready for a conversation around financial planning. Most others simply are not in that headspace yet.

A timing-first approach stops asking "Who should I call this week?" and asks instead "Who on my list has recently experienced something that makes them likely to need guidance right now?" That question produces a shorter, higher-value list. Timing is what moves people from "not now" to "let's talk."

The question is not just timing. It is also knowing which prospects belong in your financial advisor target market well enough that any wealth event becomes a relevant signal.

2. Target wealth events that create urgency

Not all life events are equal from a prospecting standpoint. The relevant ones create new wealth, reshape existing wealth, or trigger questions the prospect does not already have an answer to:

Career and income events

- Job change to an executive role. New equity packages, deferred comp, and compensation structures introduce complexity that often outpaces a prospect's existing advisory relationship.

- Company acquisition or merger. These trigger stock vesting, accelerated options, or sudden liquidity. The window between announcement and close is when attentive advisors can get in front of affected employees.

Liquidity events

- Business sale or exit. For most founders, this is the largest single wealth event of their life. The proceeds need to go somewhere quickly, and the prospect is acutely aware they need guidance.

- IPO participation or pre-IPO equity. Advisors who surface before the lockup period expires are in a different conversation than those who show up after.

Real estate and wealth transfer

- Property sale. A prospect who just sold a second home or an investment property is actively thinking about reinvesting or managing that capital.

- Inheritance or estate transfer. Emotionally complex and high-stakes. Prospects who inherit significant assets are often doing it for the first time and are genuinely unsure who to trust.

Cerulli Associates projects $124 trillion in wealth will transfer between generations over the next 25 years.

Advisors who build systems around identifying these moments early are positioned very differently than those who find out after the fact, a principle that applies directly to high-net-worth prospecting.

3. Time every channel around the event

Warm introductions, LinkedIn outreach, referral asks to CPAs and estate attorneys, follow-up sequences: all of these methods still work. What changes is the trigger for using them.

Warm introductions with specific event context

A warm introduction becomes a lot more specific when you come in with context: "I noticed your former colleague just moved into a CFO role. Would you be comfortable making an introduction?" That is a different conversation than a general referral ask. The client has something concrete to respond to, and the prospect already has a reason to pay attention.

LinkedIn outreach timed to prospect milestones

Connecting with someone the same week they announce a new role or a company milestone means you are showing up when they are already thinking about transitions. Your message does not land like a cold pitch.

COI referral asks framed around specific events

When you ask a CPA or estate attorney for introductions, you are usually asking them to scan their entire client base. When you ask specifically about clients who recently experienced a qualifying event, like a business sale or an inheritance, you are giving them a much more specific question to answer, and you are more likely to get a name.

The COI relationships most worth building are the ones covered in referral sources for financial advisors, professionals who already intersect with your ideal client at the moment a wealth event occurs.

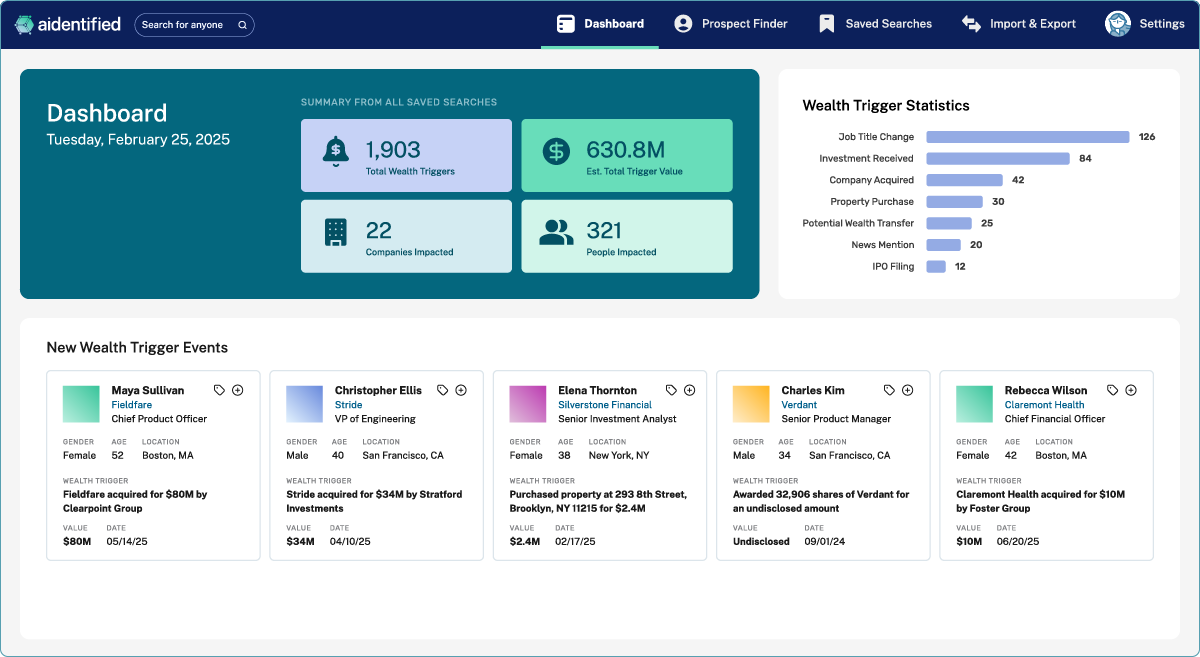

4. Monitor your prospect list for wealth events at scale

Knowing which events matter is the theory. The practical question is how you find out when they happen for people on your list, and that comes down to which tools for financial advisors you're actually using to track it. There are a few levels to this, and they are worth distinguishing because the difference in scale is significant.

1. Manual monitoring

Google Alerts, regular LinkedIn checks, scanning local business press. This works for 20-30 names. Beyond that, it becomes a part-time job with a lot of gaps.

2. CRM-based tracking

CRM tracking is better than manual, but it is still dependent on information you already have. If a prospect on your list sells their business quietly or has some other liquidity event and you are not in their immediate circle, you will not know.

3. Data-driven monitoring

Platforms that monitor wealth events across a large database flag when someone in your prospect universe hits a qualifying moment. The most capable combine relationship intelligence data with sales intelligence tools to surface not just the event but the warmest path to the prospect.

5. Check timing before every outreach

Before sending any prospecting outreach, run through this:

- Has an important wealth event occurred for this prospect recently? If not, hold. A well-crafted message to someone who is not in motion is still noise.

- What type of event was it, and what financial need does it most likely create? A business sale creates different questions than a job change. Tailor your angle accordingly.

- Do you have a warm path to this person? Check your network and your clients' networks before going cold. A single shared connection changes the entire dynamic.

- If you have a warm path, approach the mutual connection with the specific context, not "do you know anyone who needs a financial advisor," but "your former colleague just had X happen, would you be open to making an introduction?"

- If there is no warm path, lead your message with the event, not your credentials. The prospect already knows there are financial advisors. What they do not know is that you are aware of their situation and have relevant experience.

Put these financial advisor prospecting ideas to work with Aidentified

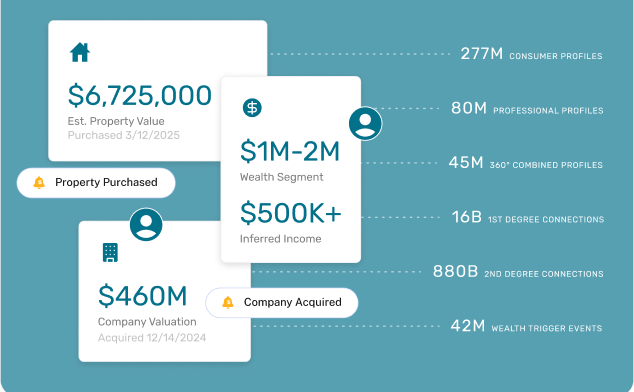

The timing-first approach works. The bottleneck is that manually tracking wealth events across a full prospect list eats the approach. As prospecting software for advisors, Aidentified monitors 300M+ profiles across 16 wealth event types and maps the warm introduction path already inside your network.

{{banner}}

FAQ: Do you have any questions?

Reveal the power of your network with Aidentified’s industry-leading AI.

Discover how Aidentified can transform your specialty services business. Contact us today for a personalized consultation and demo.

Explore a demo