8 Prospecting strategies for financial advisors across every wealth segment

Download the LLM 2026 Prompting Guide

Teach your AI to think like your firm with 10+ customizable prompts

Download TodayTL;DR

Activity-based prospecting, more calls, more emails, more outreach, produces diminishing returns in financial services because it ignores timing.

Wealth events create short windows of genuine receptivity. The advisor who arrives during that window has a fundamentally different conversation than one who arrives cold.

The highest-converting prospecting channel is a specific warm introduction from a trusted mutual connection, made at the moment of a wealth event.

COI partnerships position advisors earlier in the decision window than almost any other channel, because the referring professional sees the event as it happens.

Most prospecting advice for financial advisors focuses on doing more: more calls, more LinkedIn messages, more emails, more content. The implicit promise is that sufficient volume eventually produces results.

That framing misses the most important variable. The advisors who build practices consistently are not necessarily doing more prospecting. They are prospecting at the right moment, when a prospect has recently experienced a financial event that makes them actively receptive to advisory guidance. The same outreach effort applied to a timed opportunity versus a cold list produces results that are not comparable.

These eight strategies are built around that insight. They cover how to identify the right prospects, how to find warm paths to them, and how to time outreach to the moments that matter. Advisors who want to build a systematic financial advisor prospecting pipeline need both the strategy and the advisor prospecting software that makes timing visible. Start with warm leads for financial advisors already in a decision window rather than building from cold, or browse a broader set of financial advisor prospecting ideas to see which approach fits your book.

Why most financial advisor prospecting tips produce inconsistent results

Most prospecting strategies for financial advisors are borrowed from B2B sales playbooks designed for teams selling software or services to companies. Those playbooks optimize for activity volume and pipeline coverage because the buyer universe is large and the conversion at any given moment is roughly predictable.

Financial advisory is not like B2B software sales. Conversion is not roughly predictable based on activity volume, it is heavily dependent on timing. A qualified prospect who has not recently experienced a financial event is not a prospect. They are a contact who might become one someday. The right framework is not "how do I reach more people" but "how do I identify who in my target market has recently entered a decision window and find the fastest warm path to them." See how financial advisor lead generation strategies change when built around event detection rather than contact volume.

8 Prospecting strategies for financial advisors built around wealth events and warm introductions

These strategies are not equally weighted. The first four operate on the highest-probability channels and are ordered by the strength of the trust signal each one carries. The final four amplify and systematize the first four at scale.

1. Build a defined target market before any prospecting begins

Unfocused prospecting is the most common reason advisory pipelines stay thin. When every outreach is calibrated for a different type of prospect, none of it is precise enough to resonate, and the wealth events that create receptivity windows cannot be monitored without knowing whose events to watch.

Defining a target market, by wealth level, life stage, industry, and geography, gives every prospecting decision a filter: which second-degree connections to pursue, which COIs to cultivate, and which wealth events to monitor. A defined target market is not a constraint on growth. It is the precondition for making every other strategy on this list work. See how how to get clients as a financial advisor changes when all channels are aligned to a defined segment.

2. Map your second-degree network before building a cold list

Your existing clients are already connected to the prospects you want to reach. Before building any cold outreach list, map what your current book actually contains in terms of second-degree connections. For each of your top twenty or thirty clients, identify the people they know who fit your target market: former colleagues, business partners, fellow board members, or close professional contacts approaching a financial transition.

Most advisors discover they have direct warm paths to dozens of qualified prospects they have never approached. That is a higher-probability pipeline than any cold list, and it requires no acquisition cost to build. See how how to grow your client base as a financial advisor starts with the network that already exists before adding new prospecting channels.

3. Prospect around wealth events, not demographic profiles

The single most effective timing lever in financial advisor prospecting is the wealth event. These are the moments when a prospect's financial situation has changed in ways their existing advisory relationships may not be equipped to handle, and when the need for guidance is immediate rather than theoretical.

The events that consistently open advisory windows include:

- Business sales and liquidity events, where proceeds require placement and immediate tax planning

- Equity vesting or company acquisitions, particularly for executives with concentrated positions

- Senior role changes into titles with complex compensation for the first time

- Significant inheritance or estate settlement

- Divorce or widowhood, where existing financial relationships need restructuring

The event is what makes outreach timely rather than intrusive. Advisors who arrive through a warm introduction during a wealth event window have a fundamentally different conversation than those who arrive cold. See how prospecting high-net-worth clients changes when event monitoring replaces static demographic screening. For a broader set of tactics built on the same principle, these financial advisor prospecting ideas rank prospects by event readiness rather than list order.

4. Make specific introduction asks tied to a named prospect and a reason

The introduction ask is where most advisors lose the opportunity. A general request, "if you know anyone who might benefit from working with me," gives the client an impossible task: scanning their entire social network against a vague criteria set. Most will nod and do nothing. Not because they are unwilling, but because there is nothing specific enough to act on.

The ask that converts is specific. It names a prospect, provides context, and gives the client one clear action: "I noticed your former colleague recently sold their stake in their company. If you have stayed close, I would welcome an introduction when the timing feels right. I am happy to draft a note you could forward." Specificity transforms a vague request into a single yes-or-no decision, which most clients with a strong relationship will answer yes. See how best referral sources for financial advisors are activated through specific, contextual asks rather than generic referral programs.

5. Build COI partnerships with professionals who see wealth events first

Attorneys, accountants, and estate planners interact with clients precisely when wealth events occur. An M&A attorney is present at the start of a business sale. A CPA meets an executive at the moment retirement income decisions are being made. These professionals see the event as it happens, which positions them earlier in the decision window than most financial advisors ever naturally get.

Building COI relationships takes time and genuine value exchange: share useful information, make introductions yourself, and demonstrate expertise with the same type of client. A COI referral carries stronger implied trust than almost any other introduction path because the referring professional's credibility transfers directly to you. See how best referral sources for financial advisors includes COI development as the highest-leverage long-term prospecting channel.

6. Use LinkedIn as a credibility layer, not a primary outreach channel

LinkedIn is most effective as the thing a referred prospect checks before responding, not the channel that generates the introduction. A focused presence demonstrating expertise in your target market serves as credibility insurance for every warm introduction you generate. Cold outreach through LinkedIn converts poorly for the same reason cold email does: no prior trust relationship. See how financial advisor prospecting treats LinkedIn as a conversion layer rather than a primary pipeline source.

7. Segment your outreach by prospect readiness, not by contact type

Not all prospects in your pipeline are at the same stage, and treating them with the same outreach cadence wastes capacity on the second group and under-serves the first. Prospects in an active wealth event window get proactive, specific outreach. Qualified-but-not-yet-triggered prospects get light maintenance contact. All high-effort outreach is concentrated on the moments that actually convert. See how wealth management prospecting tools support this segmentation at the data layer.

8. Use relationship intelligence to scale event-driven prospecting beyond manual capacity

The first seven strategies work individually. The constraint is that manual prospecting, mapping networks, monitoring for events, and maintaining a segmented pipeline, has a ceiling. Once a book reaches twenty or thirty clients, maintaining a current picture of who those clients know and which of their connections have recently experienced a wealth event becomes practically impossible without the right digital tools for financial advisors in place. This is usually the point where advisors start looking for more efficient ways to generate financial advisor leads instead of relying on manual tracking alone.

Relationship intelligence platforms solve both problems simultaneously. They map connections between your clients and a defined target market, score those connections by strength and recency, and monitor for the wealth events that indicate when a prospect has entered a decision window. The result is a prospecting workflow where the right prospect, through the strongest available introduction path, surfaces at the moment of genuine receptivity rather than at random. See how AI tools for financial advisors layer wealth event intelligence on top of relationship mapping to make this systematic.

Comparing the range of financial advisor tools available, alongside broader client acquisition strategies, makes clear how much variance exists in event detection accuracy and connection mapping depth.

How Aidentified makes financial advisor prospecting event-driven at scale

Most advisors already understand that warm introductions outperform cold outreach and that timing matters. What they lack is visibility into when the timing is right and which introduction path to use. The strategies above change fundamentally when the data infrastructure behind them is built around wealth events and relationship intelligence rather than contact volume.

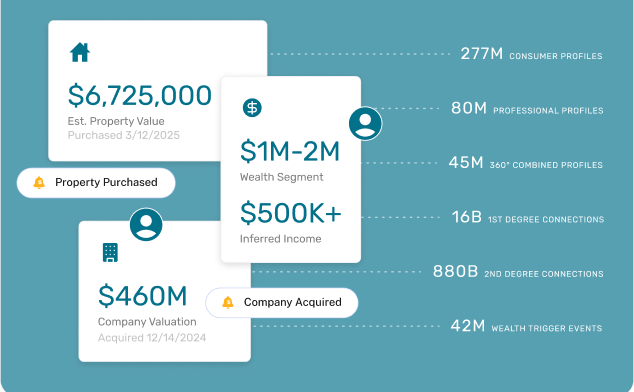

Aidentified monitors 300M+ profiles, maps 16B+ connections, and tracks 16 wealth event types. When a prospect in your defined target market experiences a qualifying event, it surfaces the strongest warm introduction path from your existing network at that moment, giving you a specific, timely ask to make rather than a cold list to work through. CRM integrations with Salesforce, HubSpot, Redtail, Lofty, and Wealthbox mean the intelligence flows directly into your existing workflow without a parallel system to manage. For a closer look at the AI layer behind this, see our ai for financial advisors guide.

If you are ready to see how event-driven prospecting works in practice, try Aidentified for free.

FAQs: prospecting strategies for financial advisors

What is the most effective prospecting method for financial advisors?

A warm introduction from a trusted mutual connection, made at the moment a prospect has recently experienced a wealth event, consistently outperforms every other prospecting method. The combination of a trust transfer from the introducing party and a genuine financial need from the prospect creates the conditions for a conversation that cold outreach almost never produces.

Most advisors know this in principle but lack the visibility to execute it systematically. They cannot see which clients are connected to which qualified prospects, or which of those connections have recently experienced an event. Relationship intelligence platforms address both gaps, making the highest-converting method repeatable rather than occasional. See how financial advisor prospecting changes when event detection drives the introduction ask.

How many prospects should a financial advisor have in their pipeline?

Pipeline size matters less than pipeline quality. Twenty qualified prospects, each reachable through a warm introduction path during a wealth event window, outperform two hundred cold contacts sorted by demographic profile.

The practical implication is that advisors should invest in pipeline quality, not pipeline volume. Monitoring for wealth events within a defined target market produces a smaller but far more actionable pipeline than list-building from demographic criteria alone. See how how to grow your client base as a financial advisor connects pipeline quality to conversion rate rather than to volume.

How do financial advisors prospect without cold calling?

The most effective alternatives to cold calling are all warm-channel strategies: specific introduction asks through existing clients, COI referrals from attorneys and accountants who see wealth events first, LinkedIn presence that supports warm introductions, and event-triggered outreach where a wealth event provides the natural reason for contact.

None of these require cold calling because the trust signal is already present before outreach begins. The challenge is building the network density and event monitoring capability to deploy them consistently. See how how to get clients as a financial advisor structures warm-channel prospecting into a repeatable system.

What data do financial advisors use for prospecting?

The data that drives effective financial advisor prospecting is not the same as standard B2B contact data. Professional titles, company information, and email addresses are useful for basic contact hygiene but do not answer the questions that actually determine prospecting decisions: does this prospect have sufficient financial complexity, have they recently experienced a wealth event, and who in my network can make a warm introduction?

Effective prospecting data for financial advisors includes household wealth estimates, wealth event monitoring, relationship connection mapping, and property and business ownership records. These are the layers that tell you not just who a prospect is but whether and when to reach out. See how wealth management prospecting tools cover the data layers that standard contact databases leave out.

growth engine with the

LLM Prompting Guide.

Reveal the power of your network with Aidentified’s industry-leading AI.

Discover how Aidentified can transform your specialty services business. Contact us today for a personalized consultation and demo.

Explore a demo